- Overview of the Thai Market

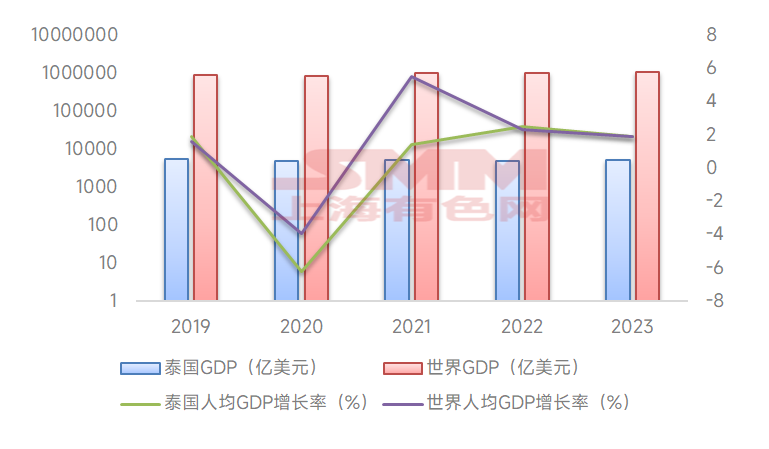

Thailand is located at the center of ASEAN, with significant geographical advantages. The country is generally socially stable, with high policy transparency and a high degree of trade liberalization. Its business environment is open and inclusive, making it the second-largest economy in ASEAN. In 2023, the global GDP reached $10.5435 trillion, up 2.72% YoY; Thailand's GDP was $514.945 billion, an increase of $19.3 billion from the previous year. The global per capita GDP in 2023 was $13,138.3, while Thailand's per capita GDP was $7,171.81, up $258.76 from the previous year. Thailand's GDP growth rate in 2024 is expected to be 2.5%, lower than the median forecast of 2.7% but higher than the revised 2023 growth rate of 2%.

Figure 1 - GDP of Thailand and the World

Source: World Bank, SMM

- Steel Supply in Thailand

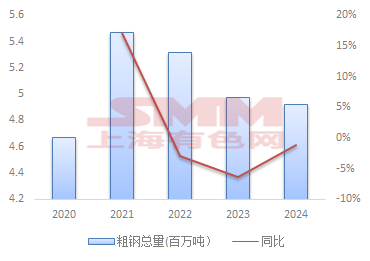

According to statistics released by the World Steel Association, Thailand's crude steel production in 2024 is expected to be 4.918 million mt, down 1.17% YoY, ranking 27th globally and fourth among ASEAN countries, following Vietnam, Indonesia, and Malaysia.

Figure 2 - Thailand's Crude Steel Production and YoY Changes, 2020-2024

Source: WSA, SMM

Thailand's steel industry consists of midstream and downstream enterprises. Midstream enterprises produce and process intermediate steel raw materials, including flat steel billets (slabs) and long steel billets (blooms), most of which rely on imports. Downstream enterprises process intermediate steel products into various shapes through hot rolling, cold rolling, coating, or forming processes (e.g., hot/cold-rolled steel, coated/electroplated steel, rebar, and various structural steels), becoming producers of downstream products.

Thailand's steel capacity is approximately 17 million mt, with over 90% of production using electric arc furnace (EAF) technology, except for Tata Steel. Major steel companies in Thailand include G Steel (1.6 million mt), GJ Steel (1.5 million mt), and Tata Steel (Thailand) (1.4 million mt). In December 2021, Nippon Steel announced a $419 million investment to acquire 49.99% of G Steel and 40.45% of GJ Steel. Singapore-based steel manufacturer Meranti plans to establish Southeast Asia's first green flat steel mill in Thailand, expected to commence operations in 2027 with an annual capacity of 2 million mt, which will increase the total steel capacity.

Table 1 - Major Steel Producers in Thailand

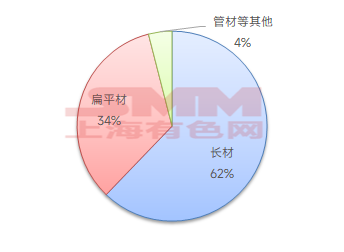

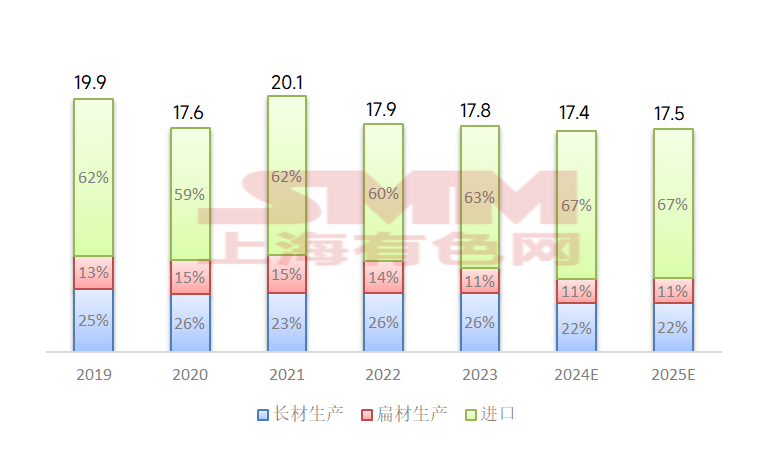

In terms of finished steel structure, in 2024, long steel is expected to account for about 62% of Thailand's total domestic steel production, flat steel about 34%, and pipes and others about 4%.

Figure 3 - Structure of Finished Steel in Thailand

Source: ISIT, SMM

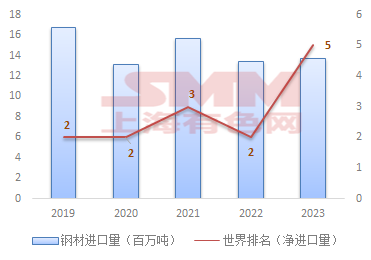

Thailand's steel industry has been impacted by Chinese steel enterprises entering the ASEAN market for over a decade, leading to a continuous decline in local capacity. In 2024, Thailand's crude steel production is expected to be 4.918 million mt, with a crude steel capacity of approximately 17 million mt, resulting in a capacity utilization rate of only 29%, far below the 35-40% range seen from 2016 to 2021. The extremely low capacity utilization rate means that local steel supply cannot meet domestic demand, making Thailand highly dependent on imports. In 2023, Thailand ranked as the world's 9th largest steel importer with imports of 13.7 million mt; its net imports reached 12 million mt, ranking fourth globally after the US, Egypt, and Mexico.

Figure 4 - Thailand's Steel Imports and Global Net Import Rankings, 2019-2023

Source: WSA, SMM

From 2019 to 2023, Thailand's domestic steel production averaged about 7.5 million mt annually, with 70% of long steel production used in construction and 30% of flat steel production used in construction, automotive manufacturing, various components, and appliances. Over the past five years, Thailand's annual steel imports averaged 14.52 million mt, accounting for 63% of domestic steel supply. Due to cost structures and the lower prices of foreign steel, Thailand's steel imports have shown a continuous upward trend.

By 2025, Thailand's domestic steel production is expected to reach approximately 5.8 million mt, mainly driven by increased long steel production (+0.8%) supported by domestic construction activities. Meanwhile, flat steel production will continue to face competitive pressure from Chinese steel, with overall steel supply coming from both domestic production and imports.

Figure 5 - Thailand's Steel Supply Over the Past 7 Years (Million mt)

Source: ISIT, SMM

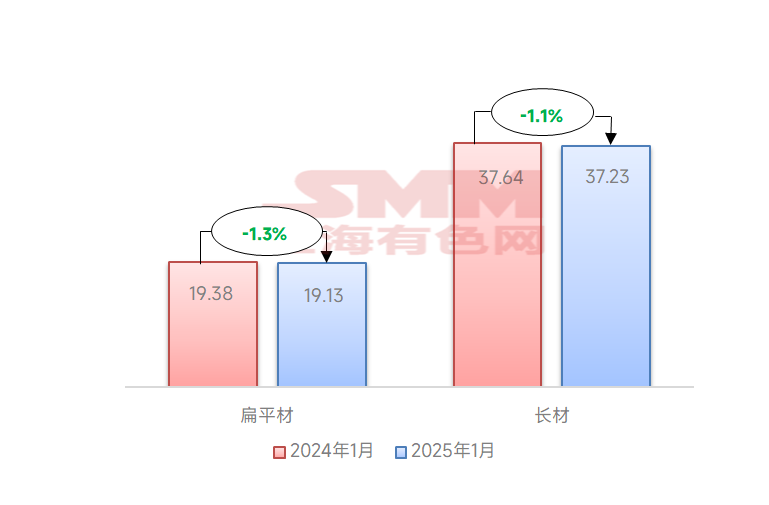

According to the Iron and Steel Institute of Thailand (ISIT), due to growing imports, Thai steel manufacturers reduced finished steel production in January, producing a total of 563,564 mt, down 1.2% YoY. This includes 372,304 mt of long steel and 191,260 mt of flat steel.

Figure 6 - Thailand's Flat and Long Steel Production in 2025 (10,000 mt)

Source: ISIT, SMM

Due to space limitations, Thailand's steel demand and import/export situation will be discussed in the next article.

SMM provides real-time tracking of steel import and export news. For more information, please follow the SMM official account!

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)